PowerSpectralDensity

PowerSpectralDensity[data,ω]

estimates the power spectral density for data.

PowerSpectralDensity[data,ω,sspec]

estimates the power spectral density for data with smoothing specification sspec.

PowerSpectralDensity[tproc,ω]

represents the power spectral density of a time series process tproc.

Details and Options

- PowerSpectralDensity is also known as the energy spectral density.

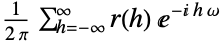

- PowerSpectralDensity[tproc,ω] is defined for weakly stationary time series processes as

, where

, where  denotes CovarianceFunction[proc,h].

denotes CovarianceFunction[proc,h]. - The following smoothing specifications sspec can be given:

-

c use c as a cutoff w use a window function w {c,w} use both a cutoff and a window function - For a window function w and positive integer c, PowerSpectralDensity[data,ω,{c,w}] is computed as

, where

, where  is defined as CovarianceFunction[data,h].

is defined as CovarianceFunction[data,h]. - By default, the cutoff c is chosen to be

, where

, where  is the length of data, and the window function is DirichletWindow.

is the length of data, and the window function is DirichletWindow. - A window function

is an even function such that

is an even function such that  ,

, ![TemplateBox[{{w, (, x, )}}, Abs]<=1](Files/PowerSpectralDensity.en/9.png "TemplateBox[{{w, (, x, )}}, Abs]<=1") ,

,  for

for ![TemplateBox[{x}, Abs]>1/2](Files/PowerSpectralDensity.en/11.png "TemplateBox[{x}, Abs]>1/2") , including standard windows such as HammingWindow, ParzenWindow, etc.

, including standard windows such as HammingWindow, ParzenWindow, etc. - A window function can be given as a list of values {w0,…}, where

, and it will be applied symmetrically in the vector case.

, and it will be applied symmetrically in the vector case. - PowerSpectralDensity takes the FourierParameters option. Common settings for FourierParameters include:

-

{1,1}

default setting {-1,1}

often used for time series {a,b}

general setting

Examples

open all close allBasic Examples (3)

Estimate the power spectral density for some data:

PowerSpectralDensity[Range[10], ω]Calculate the power spectral density for a univariate time series:

PowerSpectralDensity[ARProcess[{a}, σ^2], ω]The sample power spectral density for a random sample from autoregressive time series:

data = RandomFunction[ARProcess[{.2}, .1], {1, 1000}];Calculate power spectral density with cutoff:

cutoffs = {5, 10, 17};

spec = Table[PowerSpectralDensity[data, ω, i], {i, cutoffs}];Plot[Evaluate@spec, {ω, -π, π}, PlotLegends -> cutoffs]Scope (14)

Empirical Estimates (4)

Estimate the power spectral density for a univariate time series:

data = TemporalData[TimeSeries, {{{-0.0614065187043199, 2.6306604608936857, 3.9465133828074777,

3.745705410210661, 3.049768958525431, 1.4003183889805526, -0.755044374280679,

-2.0834316975526366, -1.3583280202011117, 0.14932145182161072, -0.8588219015885377}},

{{0, 10, 1}}, 1, {"Continuous", 1}, {"Discrete", 1}, 1,

{ValueDimensions -> 1, ResamplingMethod -> None}}, False, 10.1];PowerSpectralDensity[data, ω]Plot[%, {ω, -π, π}, Filling -> Axis, PlotRange -> All]Power spectral density for a vector time series:

data = TemporalData[TimeSeries, {{{{-0.8805412843977076, 0.5330873177260956},

{-1.091904325250007, 2.8824771870568764}, {0.4712280848587277, -2.563788099997642},

{-1.0458566604266817, 1.2863067750997783}, {0.15937341588902115, 0.0582751907559111 ... 0441, -1.4624411116452787},

{-1.2038000803608786, 0.6266434204415561}, {-1.5532848855025663, -1.4784686973103551}}},

{{0, 10, 1}}, 1, {"Continuous", 1}, {"Discrete", 1}, 2,

{ValueDimensions -> 2, ResamplingMethod -> None}}, False, 10.1];psd = PowerSpectralDensity[data, ω]//SimplifyPower spectral density for each component:

Table[Plot[psd[[i, i]], {ω, -π, π}], {i, 1, 2}]Cross power spectral density between components:

Table[ParametricPlot[{Re[#], Im[#]}&@psd[[i, Mod[i, 2] + 1]], {ω, -π, π}, ColorFunction -> Function[{x, y, ω}, (ColorData["Rainbow"][ω])]], {i, 1, 2}]Estimate the power spectral density for an ensemble of paths:

data = RandomFunction[ARProcess[{.8}, 1], {0, 100}, 5];psd = PowerSpectralDensity[data, ω];Plot[psd, {ω, -π, π}, PlotRange -> All, Filling -> Axis]Compare empirical and theoretical power spectral densities functions:

proc = MAProcess[{.4, .3, .5, .6, .3}, 1.];data = RandomFunction[proc, {0, 10 ^ 2}];Plot[#, {ω, -π, π}, Filling -> Axis, PlotRange -> All]& /@ {PowerSpectralDensity[proc, ω], PowerSpectralDensity[data, ω]}Smoothing (5)

Obtain a smoothed estimate using a cutoff at 5:

data = Range[10];sspec = PowerSpectralDensity[data, ω, 5]Compare the smoothed spectrum to the original:

Plot[{Evaluate@PowerSpectralDensity[data, ω], sspec}, {ω, -π, π}, Filling -> Axis, PlotRange -> All]Compute the power spectral density using a NuttallWindow:

data = Range[10];sspec = PowerSpectralDensity[data, ω, NuttallWindow]Compare the smoothed spectrum to the original:

Plot[{Evaluate@PowerSpectralDensity[data, ω], sspec}, {ω, -π, π}, Filling -> Axis, PlotRange -> All]Define a window using a pure function:

data = Range[10];sspec = PowerSpectralDensity[data, ω, HannPoissonWindow[#, (1/2)]&]Compare the smoothed spectrum to the original:

Plot[{Evaluate@PowerSpectralDensity[data, ω], sspec}, {ω, -π, π}, Filling -> Axis, PlotRange -> All]Estimate the power spectral density using specified window function values:

n = 10;

data = Range[n];

win = TukeyWindow[(#/2 * (n - 1)), (1/3)]& /@ Range[0, n - 1];Compare to power spectral density with explicit TukeyWindow:

PowerSpectralDensity[data, ω, win] === PowerSpectralDensity[data, ω, TukeyWindow]Compare the smoothed spectrum to the original:

Plot[{Evaluate@PowerSpectralDensity[data, ω], Evaluate@PowerSpectralDensity[data, ω, TukeyWindow]}, {ω, -π, π}, Filling -> Axis, PlotRange -> All]Compute the power spectral density, given a cutoff and a window function:

data = Range[10];sspec = PowerSpectralDensity[data, ω, {5, BartlettWindow}]Compare the smoothed spectrum to the original:

Plot[{Evaluate@PowerSpectralDensity[data, ω], sspec}, {ω, -π, π}, Filling -> Axis, PlotRange -> All]Random Processes (5)

Power spectral density for an ARProcess:

proc[a_] = ARProcess[{a}, 1];Plot[PowerSpectralDensity[#, w], {w, -π, π}, Filling -> Axis, PlotRange -> All]& /@ {proc[0.8], proc[-0.8]}PowerSpectralDensity[proc[a], w]Vector ARProcess:

a = {{1 / 7, 0}, {1 / 3, 0}};

Σ = {{1, -1 / 3}, {-1 / 3, 1}};

proc = ARProcess[{a}, Σ];psd = PowerSpectralDensity[proc, ω];

psd//MatrixFormParametricPlot[{Re[#], Im[#]}&@psd[[1, 2]], {ω, -π, π}, ColorFunction -> Function[{x, y, ω}, (ColorData["Rainbow"][ω])]]Power spectral density for an MAProcess:

proc[b_] = MAProcess[{b}, 1];Plot[PowerSpectralDensity[#, w], {w, -π, π}, Filling -> Axis]& /@ {proc[0.9], proc[-0.9]}PowerSpectralDensity[proc[b], w]Vector MAProcess:

a = {{1 / 10, 0}, {1 / 3, 0}};

Σ = {{1, 1 / 3}, {1 / 3, 1}};

proc = MAProcess[{a}, Σ];psd = PowerSpectralDensity[proc, ω];

psd//MatrixFormParametricPlot[{Re[#], Im[#]}&@psd[[1, 2]], {ω, -π, π}, ColorFunction -> Function[{x, y, ω}, (ColorData["Rainbow"][ω])], AspectRatio -> 1]Power spectral density for an ARMAProcess:

proc[a_, b_] = ARMAProcess[{a}, {b}, 1];Plot[PowerSpectralDensity[#, w], {w, -π, π}, Filling -> Axis, PlotRange -> All]& /@ {proc[0.3, 0.2], proc[-0.3, -0.2]}PowerSpectralDensity[proc[a, b], w]Vector ARMAProcess:

a = {{1 / 9, 0}, {1 / 3, 1 / 2}};

b = {{1, 3 / 4}, {1 / 2, -1 / 4}};

Σ = {{1, 1 / 3}, {1 / 3, 1}};

proc = ARMAProcess[{a}, {b}, Σ];psd = PowerSpectralDensity[proc, ω];

psd//FullSimplify//MatrixFormParametricPlot[{Re[#], Im[#]}&@psd[[1, 2]], {ω, -π, π}, ColorFunction -> Function[{x, y, ω}, (ColorData["Rainbow"][ω])], AspectRatio -> 1]Power spectral density for a fractionally integrated time series:

Plot[PowerSpectralDensity[FARIMAProcess[{.3, -.2}, -.4, {1}, 1], w], {w, -π, π}, Filling -> Axis, PlotRange -> All]PowerSpectralDensity[FARIMAProcess[{.3, .2}, .4, {1}, 1], w]Vector FARIMAProcess:

a = {{1 / 9, 0}, {1 / 3, 1 / 2}};

b = {{1, 1 / 4}, {1 / 2, 0}};

Σ = {{1, 0}, {0, 1}};

proc = FARIMAProcess[{a}, {1 / 3, -1 / 4}, {b}, Σ];psd = PowerSpectralDensity[proc, ω];

psd//FullSimplify//MatrixFormParametricPlot[{Re[#], Im[#]}&@psd[[1, 2]], {ω, -π, π}, ColorFunction -> Function[{x, y, ω}, (ColorData["Rainbow"][ω])], AspectRatio -> 1]Power spectral density for a seasonal time series:

Plot[PowerSpectralDensity[SARMAProcess[{.2}, {.4}, {12, {.3}, {1}}, 1], w], {w, -π, π}, Filling -> Axis]PowerSpectralDensity[SARMAProcess[{a}, {b}, {12, {g}, {h}}, σ^2], ω]Vector SARMAProcess:

a = {{1 / 9, 0}, {1 / 3, 1 / 2}};

b = {{1 / 3, 1 / 4}, {1 / 2, 0}};

Σ = {{1, 0}, {0, 1}};

proc = SARMAProcess[{}, {b}, {4, {b}, {}}, Σ];psd = PowerSpectralDensity[proc, ω];

psd//FullSimplify//MatrixFormParametricPlot[{Re[#], Im[#]}&@psd[[1, 2]], {ω, -π, π}, ColorFunction -> Function[{x, y, ω}, (ColorData["Rainbow"][ω])], AspectRatio -> 1]Options (2)

The default value of FourierParameters:

PowerSpectralDensity[Range[10], ω, FourierParameters -> {1, 1}]PowerSpectralDensity[Range[10], ω]% - %%Change FourierParameters:

PowerSpectralDensity[Range[10], ω, FourierParameters -> {-1, 1}]It is the default value scaled:

PowerSpectralDensity[Range[10], ω]% / %%//SimplifyApplications (1)

Use power spectral density for estimating time series processes:

data = RandomFunction[ARProcess[{.3, .2}, 1], {10 ^ 3}];EstimatedProcess[data, ARProcess[2], ProcessEstimator -> "SpectralEstimator"]EstimatedProcess[data, ARProcess[2], ProcessEstimator -> {"SpectralEstimator", "Window" -> 5}]Properties & Relations (11)

Power spectral density of a time series is a transform of the CovarianceFunction:

proc = ARProcess[c, {a}, σ^2];

cf = CovarianceFunction[proc, h]ft = FourierSequenceTransform[cf, h, z]Compare to the power spectrum:

PowerSpectralDensity[proc, z]FullSimplify[% - ft]proc = ARProcess[{{{1 / 3, 11 / 10}, {1 / 5, 1 / 10}}}, {{1, 0}, {0, 1}}];cov = CovarianceFunction[proc, h]//PiecewiseExpand;fst = FourierSequenceTransform[cov, h, w]fst - PowerSpectralDensity[proc, w]//SimplifyPower spectral density of data is a transform of the sample CovarianceFunction:

sample = Range[20];

n = Length[sample];

cov = CovarianceFunction[sample, {-n + 1, n - 1}];Apply ListFourierSequenceTransform:

ListFourierSequenceTransform[cov, w, -n + 1]//SimplifyCompare to SamplePowerSpectralDensity:

PowerSpectralDensity[sample, w]//Simplify% - %%//FullSimplifyFor a vector values time series:

data = RandomFunction[ARProcess[{{{.3, .1}, {.2, .1}}}, {{1, 0}, {0, 1}}], {10}];

n = data["PathLength"];cov = CovarianceFunction[data, {-n + 1, n - 1}]["Values"];lfst = Table[ListFourierSequenceTransform[cov[[All, i, j]], w, -n + 1], {i, 1, 2}, {j, 1, 2}]PowerSpectralDensity[data, w] - lfst//Simplify//ChopPower spectrum of white noise:

FourierSequenceTransform[Piecewise[{{1, x == 0}}, 0], x, w]Compare to special case of an MAProcess:

AbsoluteCorrelationFunction[MAProcess[{}, 1], h]PowerSpectralDensity[MAProcess[{}, 1], w]Integrate to find the variance:

Integrate[PowerSpectralDensity[ARProcess[{a}, σ^2], w, FourierParameters -> {-1, 1}], {w, -π, π}, Assumptions -> σ > 0 && -1 ≤ a ≤ 1]Compare to the variance of the time series:

CovarianceFunction[ARProcess[{a}, σ^2], 0]% - %%//SimplifyIntegrate to find the sample second moment:

data = TemporalData[TimeSeries, {{{0.30013118796154015, 0.4256944865636253, -1.2546039329698115,

0.09639437311894994, -1.9173223832884778, 0.16259596973060586, -0.001109688881539693,

0.6619148052033135, 2.232751727745077, 0.06794816837802453, 1. ... 5330770230747, 0.22924102933021667, 0.1509993303482705,

-0.4613641689767734}}, {{1, 100, 1}}, 1, {"Continuous", 1}, {"Discrete", 1}, 1,

{ResamplingMethod -> {"Interpolation", InterpolationOrder -> 1}, ValueDimensions -> 1}}, False,

10.1];NIntegrate[PowerSpectralDensity[data, w, FourierParameters -> {-1, 1}], {w, -π, π}]Compare to the sample second moment:

CovarianceFunction[data, 0]% - %%//ChopPower spectral density for harmonic frequencies is related to PeriodogramArray:

data = Range[20];

n = Length[data];

spec = Table[PowerSpectralDensity[data, 2π j / n], {j, 0, n - 1}]//NCompare with PeriodogramArray:

periodogram = PeriodogramArray[data]First[periodogram] - n * Mean[data] ^ 2Rest[spec] - Rest[periodogram]//ChopDiagonal elements of the power spectral density for vector data:

data = TemporalData[TimeSeries, {{{{0.22321490696028234, -0.09955096694103477},

{-1.2036012283524826, 0.21356213785864084}, {-2.170758245872314, -2.172602353385546},

{-2.0417769517615256, -0.9854153357651101}, {-1.8679940757580273, 0.11399938753 ... 3335557631977, 1.4574116828470514}, {-0.6330195762966424, -0.6361997810358189}}},

{{0, 10, 1}}, 1, {"Continuous", 1}, {"Discrete", 1}, 2,

{ResamplingMethod -> {"Interpolation", InterpolationOrder -> 1}, ValueDimensions -> 2}}, False,

10.1];data["ValueDimensions"]psd = PowerSpectralDensity[data, ω];Compare to univariate power spectral density for each data component:

dens = Table[PowerSpectralDensity[data["Values"][[All, i]], ω], {i, 2}];Table[Plot[{psd[[i, i]], dens[[i]]}, {ω, -π, π}, PlotStyle -> {Automatic, Dotted}, PlotLegends -> {"Vector Component", "Univariate"}], {i, 2}]Power spectral density of a vector process is conjugate symmetric about zero:

proc = ARProcess[{{{1 / 3, 1 / 10}, {1 / 5, 1 / 10}}}, {{1, 0}, {0, 1}}];Conjugate /@ PowerSpectralDensity[proc, -2]PowerSpectralDensity[proc, 2]% - %%Power spectral density of a univariate process is symmetric about zero:

proc = ARMAProcess[{a}, {b}, σ^2];PowerSpectralDensity[proc, w] == PowerSpectralDensity[proc, -w]Power spectral density of a vector process is Hermitian:

proc = ARMAProcess[{{{1 / 3, 1 / 10}, {1 / 5, 1 / 10}}}, {{{1 / 8, -3 / 10}, {3 / 5, 1 / 6}}}, {{1, -.3}, {-.3, 1}}];HermitianMatrixQ[PowerSpectralDensity[proc, RandomReal[{-π, π}]]]PositiveSemidefiniteMatrixQ[PowerSpectralDensity[proc, RandomReal[{-π, π}]]]The magnitude of the sample cross spectral density is given by each component:

data = TemporalData[EventSeries,

{{{{0.4294925809742698255912415200470240013516218314553046886407`30.,

-1.7225955472058514396692544902832573500729728703324221048`30.},

{0.0548388212316276096199767991813010875210668838810634829247`30.,

0 ... 255531611908244000251642161167860416322414`30.,

0.0404300321804073415502129760700924797739015008346027682413`30.}}}, {{0, 20, 1}}, 1,

{"Continuous", 1}, {"Discrete", 1}, 2, {ResamplingMethod -> None, ValueDimensions -> 2}}, False,

10.1];data["ValueDimensions"]psd = PowerSpectralDensity[data, 3]//ChopAbs[psd[[1, 2]]] ^ 2 - Times@@Diagonal[psd]The determinant of the sample power spectral density is constant equal to zero:

FindMaximum[Abs@Det[PowerSpectralDensity[data, w]], {w, -3, 3}]Use TransferFunctionModel to calculate PowerSpectralDensity of a time series:

proc = ARMAProcess[{a}, {b}, σ^2];

psd[ω_] = PowerSpectralDensity[proc, ω]g[z_] = TransferFunctionModel[proc][z][[1, 1]]σ^2g[Exp[I ω]]g[Exp[-I ω]]//ComplexExpand//TrigExpand//Simplify% - psd[ω]//SimplifyNeat Examples (1)

Plot a product of two power spectral densities in 3D:

proc = SARMAProcess[{.2}, {.4}, {24, {.3}, {.1}}, 1];

Plot3D[Evaluate[PowerSpectralDensity[proc, w] * PowerSpectralDensity[proc, z]], {w, -π, π}, {z, -π, π}, PlotRange -> All, ColorFunction -> "IslandColors", ViewPoint -> {-3, 3, .5}]Related Links

Text

Wolfram Research (2012), PowerSpectralDensity, Wolfram Language function, https://reference.wolfram.com/language/ref/PowerSpectralDensity.html.

CMS

Wolfram Language. 2012. "PowerSpectralDensity." Wolfram Language & System Documentation Center. Wolfram Research. https://reference.wolfram.com/language/ref/PowerSpectralDensity.html.

APA

Wolfram Language. (2012). PowerSpectralDensity. Wolfram Language & System Documentation Center. Retrieved from https://reference.wolfram.com/language/ref/PowerSpectralDensity.html